Market Overview

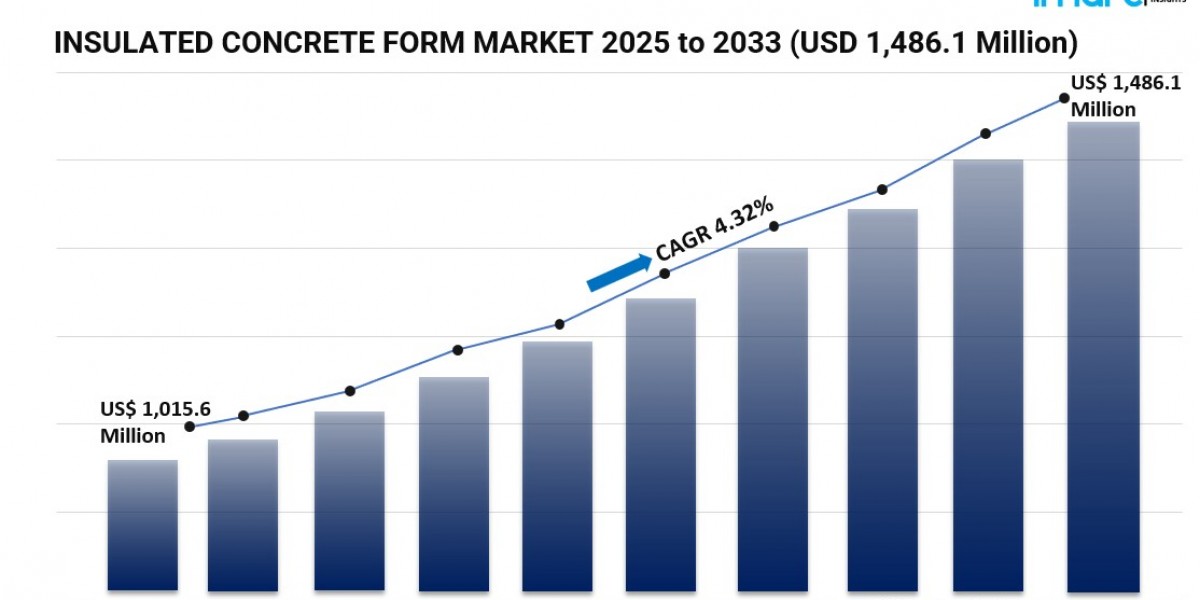

The global insulated concrete form (ICF) market reached USD 1,015.6 million in 2024 and is expected to grow to USD 1,486.1 million by 2033. This represents a CAGR of 4.32% during the forecast period 2025-2033. The market growth is driven by growing emphasis on energy efficiency and sustainability, rising disaster resilience concerns, and continuous advancements in material technology. For more details please visit the Insulated Concrete Form Market

Study Assumption Years

- Base Year: 2024

- Historical Year/Period: 2019-2024

- Forecast Year/Period: 2025-2033

Insulated Concrete Form Market Key Takeaways

- Current Market Size: USD 1,015.6 Million in 2024

- CAGR: 4.32% during 2025-2033

- Forecast Period: 2025-2033

- The increasing installation of ICFs in residential, industrial, and commercial buildings is primarily driven by their thermal, fire, and disaster resistance properties.

- Flat wall systems currently dominate the market due to their cost-effectiveness and ease of installation.

- Polystyrene foam holds the largest share among materials because of its high thermal resistance (R-value) and versatility.

- Residential end use accounts for the majority market share, fueled by continuous population growth and demand for eco-friendly living spaces.

- North America leads the market because of financial resources, proactive regulations, and the need for structures resilient to natural disasters.

Request for sample copy of this report: https://www.imarcgroup.com/insulated-concrete-form-market/requestsample

Market Growth Factors

The global Insulated Concrete Form (ICF) market is propelled by a rising emphasis on energy efficiency and sustainability within the construction industry. Builders and homeowners increasingly seek to minimize carbon emissions and environmental impact, which drives the demand for ICF systems. Regulatory bodies in various regions offer tax incentives and rebates promoting energy-efficient building practices, further catalyzing the adoption of ICF technology.

Another key growth factor is the increasing concern for disaster resilience and safety. Climate change has led to frequent severe weather events such as hurricanes and wildfires. ICF walls with a solid concrete core provide superior resistance to fire, wind, and impacts, making buildings more resilient against natural disasters. This increases the preference of architects and developers for ICF to protect occupants and infrastructure.

Advancements in ICF technology and design sustain market growth by improving construction efficiency and product performance. Manufacturers are innovating with features like built-in attachment points for electrical and plumbing systems, which reduce labor costs and streamline construction. Material improvements enhance insulation properties for better energy savings and lower environmental impacts from production processes, aligning with the global sustainability goals.

Market Segmentation

By Type:

- Flat Wall Systems

- Grid Wall Systems

- Post and Lintel Systems

Flat wall systems dominate due to their cost-effectiveness, ease of installation, reduced labor and material requirements, and flexibility to incorporate various finishes and architectural details.

By Material:

- Polystyrene Foam

- Polyurethane Foam

- Others

Polystyrene foam holds the largest share because of its high R-value (thermal resistance), cushioning properties, light weight for shipping, and the ability to be molded and shaped for diverse applications.

By End Use:

- Residential

- Non-Residential

The residential segment leads due to consistent demand for safe, secure living spaces, population growth driving new construction, stable investment opportunities, and increased eco-friendly preferences.

By Region:

- North America

- Asia Pacific

- Europe

- Latin America

- Middle East and Africa

Regional Insights

North America holds the largest market share in the insulated concrete form market. Its dominance is attributed to the availability of financial resources that enable investments in innovative construction methods and government incentives promoting energy-efficient buildings. Additionally, building codes in the region require structures to be resilient against natural disasters such as hurricanes and wildfires. These factors collectively contribute to North America's market leadership.

Recent Developments & News

- In September 2022, Amvic Inc. launched the Amvic ICF system, an expanded polystyrene (EPS) building block enhanced with graphite offering modular interlocking and flame retardance.

- In October 2020, Durisol UK commenced construction for the first phase of a new housing development in Cambridgeshire, supplying primary construction materials.

- In March 2021, Logix Brands released updated ICF engineering designs to comply with new building codes in Canada and the USA.

Key Players

- Airlite Plastics Company & Fox Blocks

- Amvic Inc.

- BASF SE

- Beco Products Ltd

- BuildBlock Building Systems LLC

- Durisol UK

- LiteForm Technologies

- Logix Brands

- Nudura Corporation (RPM International Inc.)

- Polycrete International

- Quad-Lock Building Systems

- Sunbloc Ltd.

Customization Note:

If you require any specific information that is not currently covered within the scope of the report, we will provide the same as a part of the customization.

Request for Customization: https://www.imarcgroup.com/request?type=report&id=5177&flag=E

About Us

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group,

134 N 4th St. Brooklyn, NY 11249, USA,

Email: sales@imarcgroup.com,

Tel No: (D) +91 120 433 0800,

United States: +1-201-971-6302